Social and Regulatory Risks of AI

Artificial intelligence (AI) is no longer an abstract concept; it is quickly evolving as an integrated part of our daily lives. From virtual assistants and transportation to eCommerce and even healthcare, AI is continuing to expand its application. As investors, understanding the risks and opportunities associated with this new technology is vitally important.

Since the release of OpenAI’s ChatGPT in November 2022, investors have recognised the large impact generative AI1 could have on businesses’ productivity, growth, and innovation.

In a previous article, we outlined the AI investment opportunities that we see across chip, software and cloud providers. While we have a high conviction in the structural growth tailwinds of AI, as mentioned, we must also understand the risks associated with this expansive technology. Below we focus on some of the ESG risks associated with AI and the regulatory landscape, which is evolving rapidly.

What are the ESG risks of AI?

Despite the incredible benefits that AI can bring to businesses, it comes with significant social risks – privacy concerns, bias, discrimination, misinformation, ethical considerations, job displacement, safety and autonomy to name a few.

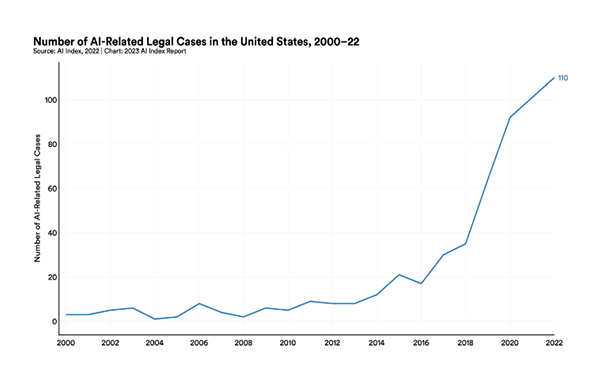

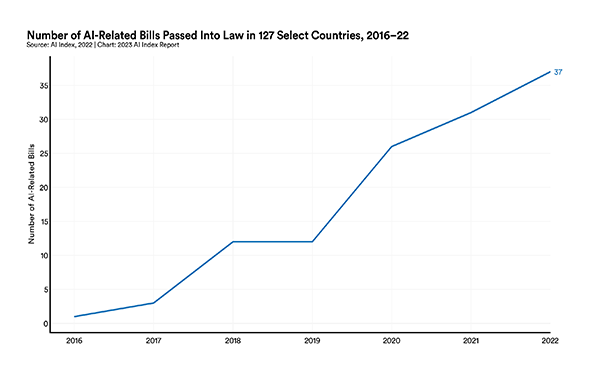

We’re already seeing rising cases of AI-related controversies, litigation and government intervention.

Source: https://aiindex.stanford.edu/report/

However, these risks should be viewed across short-, medium- and long-term horizons for a more detailed understanding of the potential impacts.

Short-term risks (within the next few years): These could include risks of misinformation, bias and inaccuracies, copyright infringement, and data breaches, security, and sovereignty. For example:

- AI has the potential to misdiagnose health issues.

- A technology platform may inadvertently distribute misinformation that could be discriminatory or fraudulent.

- AI data training sets may breach copyright, for example: The New York Times filed a lawsuit against OpenAI and Microsoft in December 2023, claiming “widescale copying” by their AI systems constitutes copyright infringement.2 Whether its allegations have merit remain to be seen.

Medium-term risks (Next 5 – 10 years): These could include risks of potential job loss, social manipulation, human rights violations and company or economic disruptions. For example:

- Automated recruitment systems may have a discriminatory bias against specific groups of people based on the data they are fed and trained on.

Long-term risks (10 years and beyond): These could include environmental or existential risks. For example:

- The increasing use of AI could lead to significantly higher energy demands, driven by the growing utilisation of computing resources.

To mitigate these risks, we have seen an increase in regulation across many jurisdictions. It’s important that both developers and users of AI technology are factoring these regulatory expectations into their intended use cases, to minimise these potential ESG risks and the potential impacts on cash flows as well as regulatory fines.

What impacts could regulatory risks have on companies?

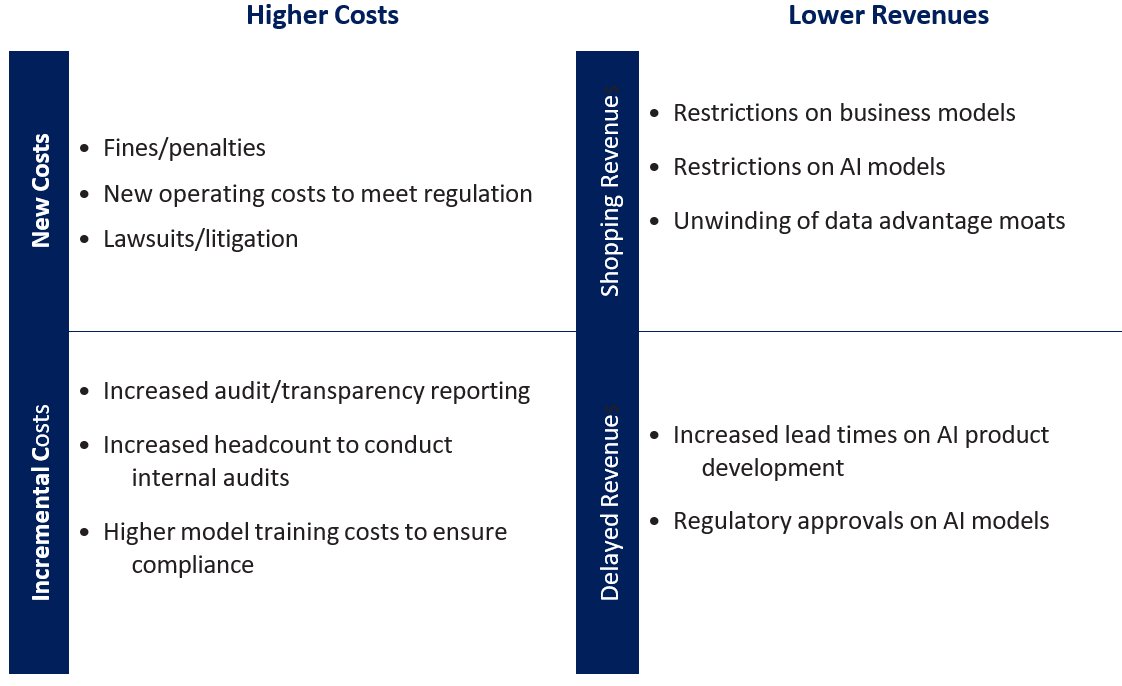

AI regulation, if not managed well, could have a negative impact on cash flows for businesses. This may come in the form of higher costs, including potential fines and litigation or increased operating costs to meet regulatory requirements. Regulation could also lead to lower revenues, with constraints on new product developments as an example.

Decreases to cash flows

What will AI regulation look like?

AI regulation has long been discussed but lags developments in technology. Early regulation targeted the short- and medium-term risks – to protect basic data rights, fundamental rights, and democratic freedoms in certain regions. An example of this was seen in New York where AI technology was created and in use for résumé screening long before the AI hiring law (under which employers who use AI in hiring must inform candidates) was implemented in New York.

Each jurisdiction is approaching AI regulation differently, ranging from self-regulation and voluntary standards to strict rules with penalties for breaches.

European Union (EU):

In April 2021, the EU proposed a risk-based framework, the EU AI Act. The use cases of AI are categorised and restricted according to whether they pose an unacceptable, high or low risk to human safety and fundamental rights. The AI Act is progressing through the process of becoming law and will sit alongside the Digital Markets Act, the Digital Services Act, the Data Governance Act and the Data Act.

United Kingdom (UK):

The UK views AI as general-purpose technology. They have proposed a principles-based regulation approach. Industry-based regulators have flexibility in how they define their own regulations with the principles as guidance.

United States (US):

Prior to the recent executive order issued by President Biden in October 2023, the US encouraged companies to follow a set of “voluntary commitments”. The new executive order grants the government greater powers to supervise how AI models are built and tested.

Australia:

Australian ministers have commented that a new advisory body would work with government, industry and academic experts to legislate AI safeguards.3

What’s next for AI and regulation?

As we have highlighted, one of the challenges of AI regulation is that the current approach is fragmented across different jurisdictions, making it more complex for companies creating or using AI to remain compliant. A way to overcome this would be the adoption of global AI standards to create consistency in how companies ensure responsible AI practices. We will continue to monitor the evolving AI regulation as well as the use of existing legislation for AI use cases such as the copyright infringement court case with The New York Times.4

What does this mean for investors?

Investors need to carefully consider the ESG risks associated with AI when making investment decisions. These risks, ranging from reputational damage to regulatory non-compliance and workforce impact, may influence the long-term growth and performance of companies. To help mitigate these risks, investors should have a detailed understanding of the companies they are investing in when it comes to their commitment to responsible AI practices. Rigorous due diligence is essential, involving thorough research and analysis of how companies approach and address social risks associated with AI. Companies that prioritise ethical considerations, engage with stakeholders and navigate regulatory landscapes effectively provide investors with greater confidence their investments are aligned with responsible business practices and are better positioned to withstand potential environmental, social and regulatory challenges associated with AI technologies.

At Magellan, social risks associated with AI form part of our company risk assessment and investment thesis. Our investment team undertakes thorough research and company engagement, and continues to monitor risks and how these risks may offset the opportunities.

Leading cloud and AI vendor Microsoft, a key exposure in our global equity portfolio, has already integrated initiatives to minimise the risk of regulation including implementing a principled approach to AI development, transparent reporting about its responsible AI learnings, an AI assurance program to bridge customer requirements with regulatory compliance, and internal governance teams integrated as part of leadership.

Expectations of companies developing AI can be summarised as:

What should AI developers be working towards to minimise risk?

- Active industry / community engagement on AI development

- Transparent reporting on developments and learnings

- Promote fairness and inclusivity in development of AI models and datasets

- Have adequate disclosures

- Internal governance teams to monitor AI risks (human oversight)

- Policies and processes to prevent AI risks like bias

- Implement AI explainability models to allow for external auditing

While some of the AI opportunities are being priced into stocks, there are still opportunities to be found, especially where companies can exploit the disruptive potential of AI. Our global equity strategies are positioned to benefit from AI growth trends through our exposure to the leading cloud and AI vendors of Microsoft, Alphabet and Amazon. ASML is well-positioned as a monopoly provider of leading-edge manufacturing equipment, while enterprise software vendors like SAP also stand to benefit.

Related reading

In a previous article, we outlined the AI investment opportunities that we see across chip, software and cloud providers. Access here.

1 Generative AI refers to algorithms that can be used to create new content based on the data they were trained on. This can include audio, images, code, text and more.

2 Boom in A.I. Prompts a Test of Copyright Law - The New York Times (nytimes.com)

3 https://www.smh.com.au/politics/federal/new-laws-to-curb-danger-of-high-risk-artificial-intelligence-20240111- p5ewnu.htm

4 Boom in A.I. Prompts a Test of Copyright Law - The New York Times (nytiWmes.com)

Important Information:

This material is not intended to constitute advertising or advice of any kind and you should not construe the contents of this material as legal, tax, investment or other advice. In making an investment decision, you should read and consider any relevant offer documentation applicable to any investment product or service and must rely on your own examination of the same and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision.

The investment program of the strategy or strategies presented herein ('Strategy') is speculative and may involve a high degree of risk. The Strategy is not intended as a complete investment program and is suitable only for sophisticated investors who can bear the risk of loss. The Strategy may lack diversification, which can increase the risk of loss to investors. The Strategy's performance may be volatile. Past performance is not necessarily indicative of future results and no person guarantees the future performance of the Strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs and such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of the Strategy or any financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. The Strategy will have limited liquidity, no secondary market for interests in the Strategy is expected to develop and there are restrictions on an investor's ability to withdraw and transfer interests in the Strategy. The management fees, incentive fees and allocation and other expenses of the Strategy will reduce trading profits, if any, or increase losses.

No representation or warranty is made with respect to the correctness, accuracy, reasonableness or completeness of any of the information contained in this material. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. The issuer of this material and its related entities and affiliates will not be responsible or liable for any losses, whether direct, indirect or consequential, including loss of profits, damages, costs, claims or expenses, relating to or arising from your use or reliance upon any part of the information contained in this material including trading losses, loss of opportunity or incidental or punitive damages.

This material and the information contained within it may not be reproduced, or disclosed, in whole or in part in any circumstances. , Further information regarding any benchmark referred to herein can be found at www.magellaninvestmentpartners.com/funds/benchmark-information/. Any third-party trademarks contained herein are the property of their respective owners and are used for information purposes and only to identify the company names or brands of their respective owners. (060126-#i1)

United Kingdom: This material has been prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners and is distributed in the United Kingdom by Magellan Investment Partners (UK) Limited (FRN: 1037936), an appointed representative of Sentinel Regulatory Services Ltd (FRN: 1007093) which is authorised and regulated by the Financial Conduct Authority. This material does not constitute an offer or inducement to engage in an investment activity under the provisions of the Financial Services and Markets Act 2000 (FSMA). This material does not form part of any offer or invitation to purchase, sell or subscribe for, or any solicitation of any such offer to purchase, sell or subscribe for, any shares, units or other type of investment product or service. This material or any part of it, or the fact of its distribution, is for background purposes only. This material has not been approved by a person authorised under the FSMA and its distribution in the United Kingdom and is only being made to persons in circumstances that will not constitute a financial promotion for the purposes of section 21 of the FSMA as a result of an exemption contained in the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (FPO) as set out below. This material is exempt from the restrictions in the FSMA as it is to be strictly communicated only to 'investment professionals' as defined in Article 19(5) of the FPO.

United States: This material has been prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners (‘Magellan’) which is a registered investment adviser. The investment strategies described herein are offered in the United States by Magellan Investment Partners North America, Inc., a U.S.-registered investment adviser. Magellan and Magellan Investment Partners North America, Inc. are affiliated entities for purposes of the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. This material is not intended as an offer or solicitation for the purchase or sale of any securities, financial instrument or product or to provide financial services. It is not the intention of Magellan to create legal relations on the basis of information provided herein. Past performance does not guarantee future results. Where performance figures are shown net of fees charged to clients, the performance has been reduced by the amount of the highest fee charged to any client employing that particular strategy during the period under consideration. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Fees are available upon request and also may be found in Part 2 of Magellan’s Form ADV.

Canada: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners (‘Magellan’). Magellan is not registered in any province in Canada. The head office of Magellan is in Sydney, Australia and all or substantially all of its assets are situated outside of Canada. Due to the foregoing, there may be difficulty enforcing legal rights against Magellan.

South Africa: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners, who in accordance with FAIS Notice 55 of 2023 issued by the Financial Sector Conduct Authority, Magellan Investment Partners is exempted from section 7(1) of the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37 of 2002). This material is not an offer in terms of Chapter 4 of the Companies Act, 2008.

UAE: This material has been produced by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. This material is not for distribution to any other person. This material, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (‘UAE’) and accordingly should not be construed as such. Any offer of securities or financial services is made only to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. No securities or services have been approved by or licensed or registered with the UAE Central Bank, the Securities and Commodities Authority, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the ‘Authorities’). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. This material is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

Japan: This material is prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. The content is for informational purposes only and directed at Qualified Institutional Investors and other professional investors as defined in the Financial Instruments and Exchange Act. No distribution of this material will be made in any jurisdiction where such distribution is not authorised or is unlawful. This material does not constitute, and may not be used for the purpose of, an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorized or in which the person making such offer or solicitation is not qualified to do so.

Other jurisdictions: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. No distribution of this material will be made in any jurisdiction where such distribution is not authorised or is unlawful. This material does not constitute, and may not be used for the purpose of, an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorized or in which the person making such offer or solicitation is not qualified to do so.